Blog

- home

- >

- Blog

The 2026 UAE Business Survival Guide: VAT Deadlines, Penalty Cuts, and New Civil Rules

Running a successful business in the UAE means you have to be adaptable. The economic landscape here moves incredibly fast, and 2026 is shaping up to be one of the most consequential years yet for commercial and tax regulations.

Whether you are running a massive retail operation, a tech startup out of a free zone, or hustling as a solo consultant, the rules of the game are changing. The Federal Tax Authority (FTA) and the UAE government have rolled out a wave of new legislation that fundamentally shifts how day-to-day business is conducted, how taxes are collected, and how penalties are enforced.

At DP Taxation Consultancy, our mission is to cut through the noise. We know that business owners don't have the time to read through hundreds of pages of dry, dense legal text. You need to know exactly what is changing, how it affects your bottom line, and what you need to do about it right now.

Let’s skip the heavy legal jargon. Here is your clear, straightforward guide to the massive UAE regulatory updates of 2026.

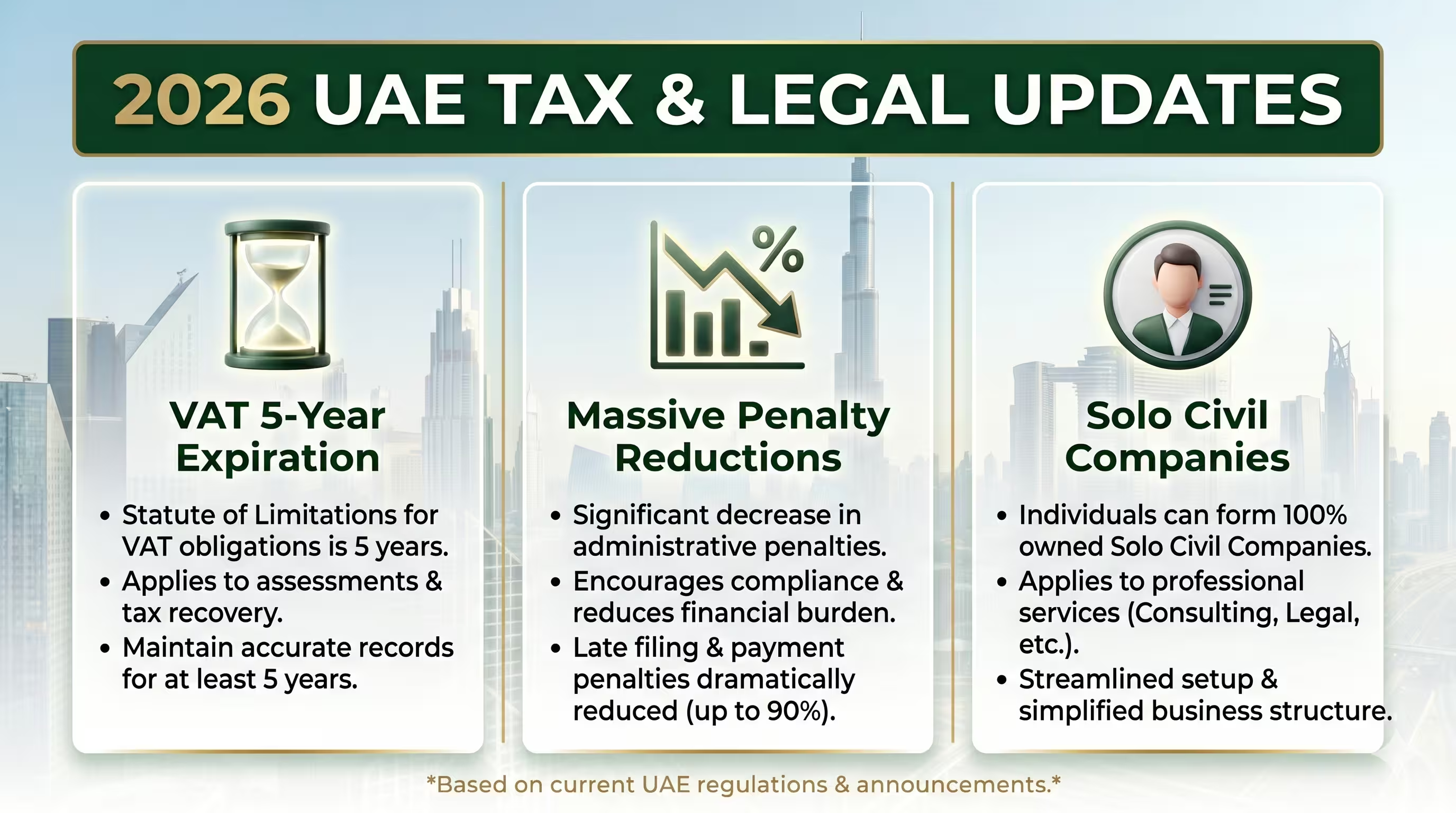

1. The 5-Year VAT Clock is Ticking: Use It or Lose It

Let's start with the most urgent update—the one that directly impacts your cash flow.

For a long time, businesses had a very comfortable safety net when it came to VAT. If you had excess VAT credits, you could essentially carry them forward indefinitely. There was no rush to claim them or apply them to your current balance.

Starting in January 2026, those old, flexible rules are officially gone. The FTA has shifted to a strict "use it or lose it" system. Moving forward, your business will have exactly five years from the end of any given tax period to formally claim your refund or utilize that credit. Once that five-year window closes, those credits permanently expire.

Why this matters right now: If your business is sitting on old, unclaimed VAT credits from back in 2021, the clock is running out. You have until December 31, 2026, to formally reconcile and claim those funds. If you miss this transitional deadline, that money will be wiped from your ledger entirely. This should be priority number one for your accounting team this quarter.

2. The Penalty Overhaul: A Massive Break for Businesses

For years, the penalty system for late tax payments has been a major pain point for UAE business owners. The old system used a compounding late fee that added 4% every single month to your outstanding balance. If a business fell behind, those penalties could spiral out of control incredibly fast, sometimes eclipsing the actual tax owed.

The government recognized this pressure, and starting in April 2026, they rolled out Cabinet Decision No. 129 of 2025. This is arguably the most business-friendly tax update we have seen in years.

No More Compounding Late Fees: The aggressive monthly compounding system has been completely scrapped. It has been replaced by a much more manageable, flat annualized rate of 14%, which accrues monthly on the outstanding tax amount.

Cheaper Administrative Mistakes: We all make paperwork errors, but they used to be incredibly expensive. Under the new rules, fines for minor administrative slip-ups have been slashed. For example, if the FTA requests a document and you fail to provide an Arabic translation, the fine used to be a staggering AED 20,000. Now? It has been dropped to just AED 5,000. Forgetting to update your FTA records has dropped from a AED 5,000 fine down to AED 1,000 for a first offense.

Forgiving Corrections: If you realize you made an honest mistake on a tax return, the penalty for correcting it is significantly lower—just AED 500 for the first violation. In many cases, if you catch and fix the error before the actual due date, the penalty can be waived entirely.

3. The New Civil Code: Single-Owner Civil Companies

Let's step away from tax for a moment and look at the structure of your business. The UAE has completely rewritten the Civil Transactions Law, dropping the old 1985 rules for a modernized 2026 framework.

One of the biggest wins in this new law is for the professional services sector. Historically, if you wanted to set up a "civil company"—which is the standard onshore setup for professional consultants, engineers, accountants, and doctors—you were legally required to have at least two partners on paper.

That barrier is officially gone. Under the new 2026 Civil Code, a single individual can fully own, operate, and manage a civil company. This offers incredible flexibility for solo professionals who want a cleaner, simpler way to structure their business without having to pull in a silent partner just to meet a legal quota.

4. The Legal Age of Adulthood Drops to 18

Another critical update in the new Civil Code is the reduction of the legal age of majority. In the UAE, the legal age of adulthood is officially dropping from 21 down to 18.

This might sound like a minor technicality, but it has massive ripple effects. It means 18-year-olds now have full legal capacity. They can legally sign binding contracts, open their own corporate bank accounts, set up their own businesses, and officially agree to your user Terms & Conditions without needing a guardian's signature.

Why this matters right now: If you run a business that deals directly with consumers—like a retail brand, a software platform, or an educational service—you need to audit your onboarding processes immediately. Your liability waivers, standard contracts, and digital terms of service need to be updated to reflect this new, younger demographic of legally binding adults.

5. Smarter, Faster Tax Procedures

Finally, the FTA has tweaked its internal administrative procedures to cut down on red tape.

Previously, if you found a minor error in a past tax return, you had to jump through the hoops of submitting a formal Voluntary Disclosure, which is a stressful and time-consuming process. Now, if you find a mistake that doesn't actually change your final tax bill (or if the excess amount is very small), the FTA allows you to simply correct the error directly on your next standard return. It’s a common-sense approach that saves everyone time.

Getting Ahead of the Curve

Dates like December 2026 might feel like they are still a ways off, but regulatory shifts of this size take time to adapt to. Auditing your consumer contracts, digging up old 2021 VAT claims, and potentially restructuring your company isn't something you can do over a weekend.

The smartest business owners in the UAE are already getting ahead of the curve and adapting their operations today.

You don't have to navigate these changes alone. Reach out to the team at DP Taxation Consultancy. We’ll sit down, review your current setup, and help you build a clear, completely jargon-free roadmap to keep your business compliant, efficient, and thriving throughout 2026.

- Dhana Pillai